Discounted Cash Flow (DCF) Valuation + Questions

Review:

If you haven't yet, go back and read the article on WACC before starting this one

Remember these formulas from the previous article:

WACC = (% Equity * Cost of Equity) + (% Preferred Stock * Cost of Preferred Stock) + (% Debt * Cost of Debt * (1 - Tax Rate))

Cost of Equity = Risk-free Rate + Levered Beta * Market Risk Premium

EV = EqV - Cash + Debt + Non-Controlling Interests + Preferred Stock

EqV = EV + Cash - Debt - Non-Controlling Interests - Preferred Stock

Introduction to Valuation

There are 2 main ways to value a company:

- Relative Valuation: using market historical data of similar companies or transactions to value a company

- Public Comps (Comparable Companies Analysis)

- Comparing the valuation multiples (such as PE ratio or EV/R ratio) of similar publicly traded companies to determine a valuation range

- Precedent Transaction Analysis

- Similar to Comps, but used more commonly in M&A scenarios. Also known as "M&A Comps"

- Analyzing recent transactions of similar businesses to assess their sale prices and using them as benchmarks

- Applies a control premium as a result of M&A transactions, so valuation will usually be higher than comps

- Intrinsic Valuation: using fundamental business characteristics and expected cash flows to value a company

- DCF

- Present value of a company's future cash flows

- There are 2 parts to a DCF:

- Projection period:

- Cash flows are projected in a typically 5-10 year period, which are then discounted and added up

- Can think of this as the "near future"

- Terminal value:

- Value of the firm beyond the forecasted projection period

- Can think of this as the "distant future"

Breaking down the DCF Analysis:

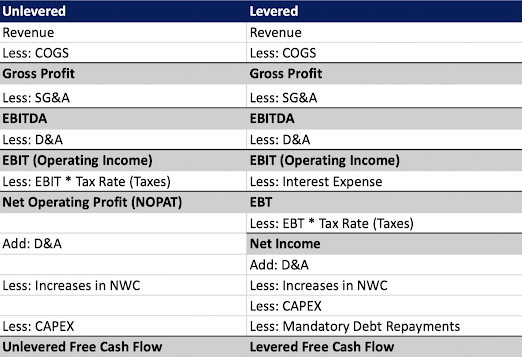

- FCF: how much after-tax cash flow the company generates on a recurring basis to its investors after we've taken into account the non-cash changes, changes in operating assets and liabilities, and required Capex.

- Free Cash Flow = Net Income + Depreciation and Amortization - Changes in Working Capital - Capex

- 2 types of FCF:

- Unlevered: cash flow available to all providers of capital, including both equity and debt holders

- Levered: available to just equity investors. Obtained after deducting interest payments, tax obligations, and required debt repayments from UFCF

- If we're using unlevered free cash flow, we use WACC as the discount rate because we care about all parts of the company's capital structure, and we will get the enterprise value

- If we're using levered free cash flow, we use cost of equity as the discount rate because we only care about equity investors, and we're calculating equity value rather than enterprise value

- Recall that UFCF indicates a company’s cash flow pre-interest expense, LFCF indicates a company’s cash flow post-interest expense

- If the company we're valuing is heavily indebted, it likely has a lot of interest expense, in which case LFCF may be a better picture of the cash flows within the company

UFCF = NOPAT + D&A + other non-cash adjustments - increase in net working capital - Capex

- UFCF = EBIT (1 - Tax Rate) - CapEx + D&A - Increase in NWC

- UFCF = CFO + Tax adjusted interest expense - CapEx

- UFCF = Net Income + Tax adjusted interest expense + D&A - Increase in NWC - CapEx

Note:

EBIT * (1 - Tax Rate) = NOPAT

"D&A" in the above equations is used as a broad proxy for non-cash expense. A more precise way of writing the formulas would be to replace "D&A" with "non-cash expense."

UFCF = NOPAT + D&A + other non-cash adjustments - increase in net working capital - Capex

I'm using the term "D&A" for simplicity purposes, because a majority of the non-cash expenses asked in interviews are D&A, and it can be sometimes forgotten that D&A is a non-cash expense.

- Project the company's revenue growth

- Assume an operating margin for the company to calculate EBIT each year

- Apply the company's effective tax rate to calculate Net Operating Profit After Tax (NOPAT)

- Add D&A because they are non-cash expense

- Estimate change in Net Working Capital (note: if NWC increases, FCF decreases)

- Subtract Capex

- The company's projected FCF is driven by assumptions of future financial performance, including sales growth rates, profit margins, Capex, and working capital requirements.

- Remember, D&A is added back because it's a non-cash expense and doesn't actually affect cash flows. If there is an increase in working capital, it represents a use of cash, while a decrease indicates a source of cash, so we subtract increases in NWC. Capex is a company's investments in acquiring, upgrading, or maintaining its long-term assets, like machinery or buildings. It represents cash outflows required to invest in the company's future growth and productivity. NOPAT is used because it represents the profit generated by a company's core operations after accounting for taxes but before considering the impact of financing decisions

- In a DCF, the simplest way is to project D&A, NWC, and Capex as % of Revenue

- There are 2 methods for calculating terminal value:

- Gordon growth / perpetual growth method

- Assume the company operates indefinitely and sum its future cash flows

- Terminal growth rate should always be very low (less than or equal the country's GDP growth rate)

- Terminal Value = Final Year Free Cash * (1+Terminal FCF Growth Rate) / (Discount Rate - Terminal FCF Growth Rate)

- Exit multiple approach

- Assume the company gets sold for a certain multiple in the future

- Terminal Value = Final Year EBITDA * EBITDA multiples

- Terminal Value needs to be discounted to Present Value using the last forecasting year's discount factor

- There is no "better" method. You almost always use both methods in a DCF to compare results

- The output at the end of a DCF tells us the company's implied share price, or equity value for private companies, across a range of assumptions

- We can then decide if the company is overvalued, undervalued, or valued appropriately

- Sensitivity tables calculate its Implied Share Price using different Terminal Value and WACC assumptions, you get a value range

- Providing a valuation range can give a reference

- Overall Impact on DCF:

- The Discount Rate and Terminal Value tend to have the biggest impact. Yes, if a company’s revenue growth rate or margins change dramatically, those could change the DCF significantly. But even a 1% increase or decrease in the Discount Rate makes far more of an impact than a 1% increase or decrease in revenue or revenue growth or EBIT margins because that Discount Rate affects everything in the analysis

- A Discount Rate difference of 1% will impact the analysis far more than a 1% increase or decrease in Terminal Value because Terminal Value is a large number, and 1% is tiny.

- Cost of Equity:

- Smaller companies, companies in emerging and fast-growing geographies and markets, usually have higher Costs of Equity because expected returns are higher

- Additional debt raises the Cost of Equity because it makes the company riskier for all investors

- Additional equity lowers the Cost of Equity because the % of debt in the capital structure changes

- Using historical vs. calculated Beta doesn't have a predictable impact - it could go either way depending on the set of comps

- WACC:

- WACC, like Cost of Equity, is also higher for smaller companies and companies in emerging and fast-growing geographies and markets

- Additional Debt reduces WACC because Debt is less expensive than Equity. Yes, Levered Beta will go up, but the additional Debt in the WACC formula more than makes up for the increase

- Additional Preferred Stock also generally reduces WACC because Preferred Stock tends to be less expensive than Equity (Common Stock)

- Higher Debt Interest Rates will increase WACC because they increase the Cost of Debt

- History

- Purpose

- Financials

- Return on Investment

- How has R&D been accounted for?

- Shareholder Agreement (if one exists)

- Value of Employees (cost of recruitment and training as a group)

- Value of Client Base and rebuild cost

- Value of Supply Chain

- Value of Distribution Network if one exists

- Internet Presence and Use (social network)

- Dominance if any in the marketplace

- Knowledge Base of Owner and Employees

- Processes, Procedures, and Systems

- Documentation (how well are all aspects of the company documented)

- Industry Averages

- Terms of lease

- Leasehold Improvements

- Equipment

- Inventory

- Risk

- Cost of Liquidation (if applicable)

- Opportunity

- Liquidity

- Leverage - Cost of money. Is leverage or applicable and if so at what risk?

- Minority Interest (if applicable)

- Special Interest Purchaser - (partners are also special interest purchasers as they have more knowledge, interest, and opportunity, with less risk than regular buyers)

- Redundancy in Management - How well is the business/practice expected to function with changes in management. (if applicable)

- Terms of Sale (if relevant) A sale with little down and the seller remaining at significant risk would demand much higher price than an all cash sale.

- Return on Investment is always our first and last consideration.

- Gordon growth:

- TV = final year FCF * (1 + growth rate) / (discount rate - growth rate)

- Exit multiples approach:

- TV = final year EBITDA * EBITDA multiple

- There is no "better" method; Gordon Growth is a more academic approach that value a company as a growing perpetuity of cash flows. And the company's growth will ultimately slow over time to around the country's GDP

- But exit multiple approach is a more practical approach, it is easy to pick an EBITDA multiple and calculate the TV

- Purpose is to find the effect of changes in operating assets and operating liabilities on cash flows

- If operating assets are increasing by more than operating liabilities, the company is spending cash and therefore reducing its cash flow

- e.g. large inventory order, sells products, and records revenue, but hasn't received cash from customers yet. Represents a use of cash

- No good comparable companies

- If multiples will change significantly in the industry several years down the road, like chemicals or semiconductors, it is better to use Gordon Growth

- Unlevered DCF is easier to set up, forecast, and explain, and it produces more consistent results than other methods

- With other methods, you have to project the company's cash and debt, net interest expense, and mandatory debt repayments

- 1% discount rate

- The discount rate and terminal value tend to have the biggest impact on a valuation

- Discount rate affects everything in the analysis

- You reflect it in a levered DCF because the company's net interest expense and debt repayments will change over time

- In levered FCF, Cost of Equity will change because additional debt increases the cost of equity and less debt reduces i

- It won't show up explicitly in unlevered FCF, but you will still reflect it in analysis by changing the discount rate over time; WACC changes as the company's debt and equity levels change

- Company that has negative or unpredictable cash flows, such as a startup

- Yes. E.g. valuing a biotech company and the patent on its key drug expires within the explicit forecast period

- Can't use DCF to value financial institutions like banks, because they have unconventional cash flows.

- The primary business model for most banks generate interest income on deposits. Unlike most other firms, they operate on both sides of the balance sheet, thus their Net Interest Income is sort of like their "revenue"

- A DCF discounts the present value of future free cash flows starting from revenue. The balance sheet (and working capital) drive the core business for banks. EBITDA is worthless here because interest is the banks' main income source

- Working capital is huge for a bank. They have tons of accounts receivables (ex., credit card income or another loan collection) and liabilities (think deposits)

- To value banks, we would need to use a dividend discount model

Comments

Post a Comment