Intro to M&A

Make sure to read the most important part at the bottom - "M&A Financing"

Types of Mergers:

- Horizontal Integration: mergers of companies in the same industry

- Vertical Integration: same production vertical but different level, e.g. tech company acquiring chips manufacturer; restaurant buying delivery service

- Conglomerates: acquiring completely unrelated businesses in different industries or geographies for diversification

Why would you buy a company?

- Consolidation - making a bunch of smaller companies into one

- Cost savings - such as from strengthened supply chain etc

- Geographic expansion

- Seller is undervalued

- Acquire new customer base or distribution channels

- Tax benefits

- Expand or diversify product lines

- Intellectual Property

- CEO ego and pride

Why would you want to get acquired?

- PE Firms or Private Businesses:

- PE firms and owners of private businesses may want to cash in their hard work after owning or operating their business for a period of time

- The alternative - IPO - is a much more difficult process. Being acquired is easier as there are less regulations and can allow for a cleaner exit, whereas most founders stay with their business after an IPO

- Public Companies:

- Mgmt may want to maximize shareholder value, and getting acquired is a quick way to create profit for shareholders

- Strategic Inventives for Both Private and Public Sellers:

- There are benefits to being acquired, especially by a bigger company, e.g. access to the buyer's intellectual property, technology, capital, and clients. These aspects can elevate our own company and bring us to new heights

Types of Buyers:

- Financial Sponsors (PE firms)

- Primary goal: generate returns from the company. Focused on increasing cash flows and usually achieve this through cost cutting

- Buy companies through LBO, and sell after few years to another buyer or IPO

- Pay less than strategic buyers as they don't capture synergies

- Strategic Buyers (Corporations)

- Primary goal: enhance the current buyer's business through the acquisition. Focused on the target company's operations

- Pay more for acquisition due to potential syngergies and strategic rationales

Types of Synergies:

- Revenue Synergies: synergies that increase revenue

- e.g. cross selling (sell a different but related product to existing customers), upselling (sell more premium products that have better margins to customers)

- Cost Synergies: synergies that decrease cost

- e.g. workforce redundancies, building consolidation (combining offices and workplaces etc), lower input costs (due to more bargaining power with suppliers to drive down cost of inputs)

Very important!

M&A Process and Financing:

Sell-side M&A Process:

- Win the mandate - so the client picks you

- Plan the process - create marketing material (teaser and CIM)

- Contact the initial set of buyers

- Set up management meetings and presentations

- Solicit initial and subsequent bids from buyers

- Conduct final negotiations and close the deal

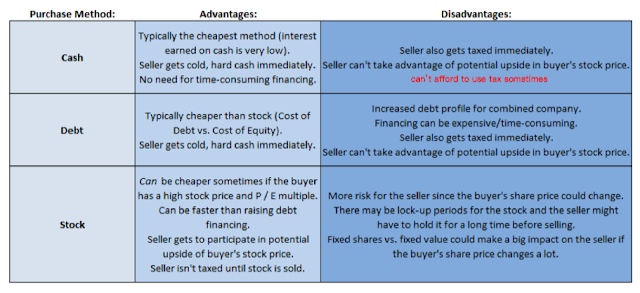

M&A Financing:

A company can use cash, debt, and/or equity to acquire other companies

- Cash:

- cheapest option - if company has excess cash on its balance sheet, it can use it for acquisitions

- cost of cash: after-tax forgone interest in cash

- Debt

- debt is cheaper than equity. using cash or debt to pay for another company is also more straightforward than using equity

- cost of debt: after-tax interest expense

- Equity

- buyer can use 2 methods: 1) issue new shares to other investors, get cash from those investors, and use that cash to pay for the seller. 2) issue shares directly to the seller in exchange for the seller's shares

- cost of equity: buyer's earnings yield (1/pe ratio of buyer). Note: cost of equity could be the lowest among the financing options if the buyer's pe ratio is extremely high

Why Most M&As Fail:

Around 80% of all M&As fail. Studies also show that for most M&As, not only do anticipated synergies never get realized, but total profits also often decrease: the M&A destroys value rather than creates it.

- Overvaluation

- Wrong acquisition rationale: the buyer's mgmt may have wanted to acquire the business as a greedy way to bolster profit growth, even when the merger may not actually be beneficial

- Cultural mismatch: the companies may have different workplace cultures. Alternatively, this mismatch may be in other areas, such as different technologies, software, team organizational structure, etc.

Comments

Post a Comment