Financing Trends & 2024 Economic Outlook

Overview:

Upside risks to inflation and downside risks to growth

Despite signaled rate cuts, interest rates are likely to stay elevated as:

Still tight monetary policy

Higher borrowing needs by US Treasury (and lower foreign demand for US Treasury bonds)

Inflation still above Fed’s 2% target

Factors unrelated to Fed policy may slow consumer spending

Households have less excess savings compared to COVID levels

Student loan payments restarting

Outlook for corporate performance

Outlook for lending

Outlook for inflation

Many are optimistic about the economy due to possible rate cuts in 2024. However, despite resilient strength in the economy, there is still more downside risk than potential upside surprise. While soft landing is not impossible, it is likely that interest rates will continue to be elevated and for longer than the market expects.

Key Trends and Analysis:

Despite signaled rate cuts, interest rates are likely to stay elevated

Even if rate cuts were to persist, they’re not gonna be 2020 levels where interest rates were basically 0%

Long-term rates are high for reasons not directly related to Fed’s monetary policy

Budget deficit forcing higher borrowing needs

Overall decrease in foreign demand for US treasuries, especially China

Chinese exports slowing = less USD to buy US treasury bonds

Factors unrelated to Fed policy may slow consumer spending

Outlook for consumer spending:

Households have less excess savings, no longer a strong tailwind

The reason why the economy hasn’t responded more dramatically to Fed rate hikes is likely because consumers refuse to stop spending

Consumer spending = 70% of GDP

During COVID, everyone had excess savings; after COVID, everyone started revenge-spending, keeping the US economy afloat

Why excess savings spiked so much: usually in a recession, people dis-save as they lose their jobs. But with COVID, there’s nowhere to spend money, so excess savings spiked in unprecedented fashion

BUT recent data has shown that Americans are running short of cash - so can expect them to become a much less powerful economic tailwind in 2024

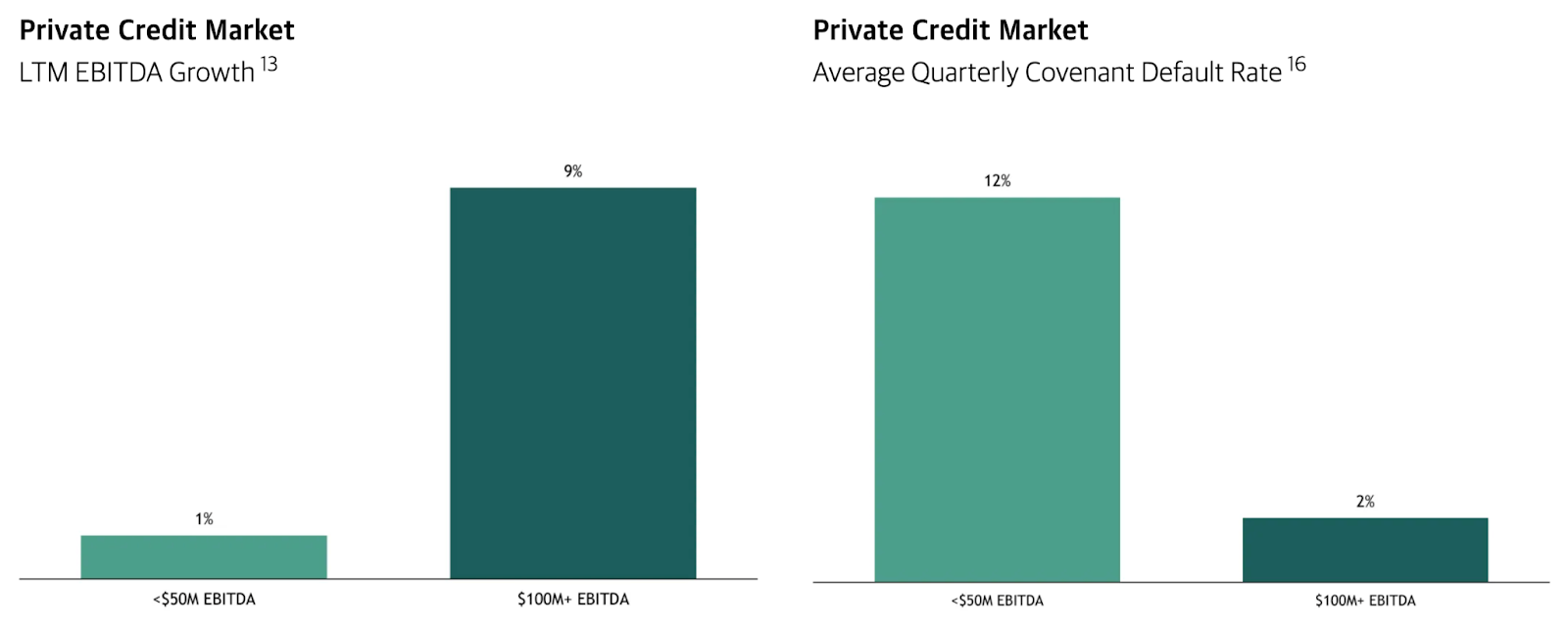

Outlook for corporate performance: beginning of a slowdown

Default rate increased after rate hike regime

Punitive environment: those already pushed to leverage line suffer first; good companies survive

Caveat is that default rates are different depending on cyclicality of industry. Cyclical sectors have 8% default rate, 2% YoY CF growth. Less cyclical sectors have 3% default rate, 5% YoY CF growth

Expect firms with lots of leverage and little cash flow to struggle

Tech and growth companies

Weaker balance sheet = more vulnerable to rising rates

Outlook for bank lending: continued slowdown ahead

When Fed raised interest rates, large banks slowed lending in anticipation of decline in credit quality; small banks kept lending until SVB happened

Since then, loan growth has slowed, giving the opportunity for private credit to come in

Given the importance of banking sector as a provider of credit in the economy, there is risk of additional negative drag on economic outlook

Outlook for inflation: still too early to declare victory

Core inflation still above Fed’s 2% target, and because of resilience in consumer spending (excess savings), inflation is not sustainably controlled yet

Month-to-month inflation has been bumpy

Outlook for interest rates: higher for longer

Central bank is starting to see cost of capital as permanently higher

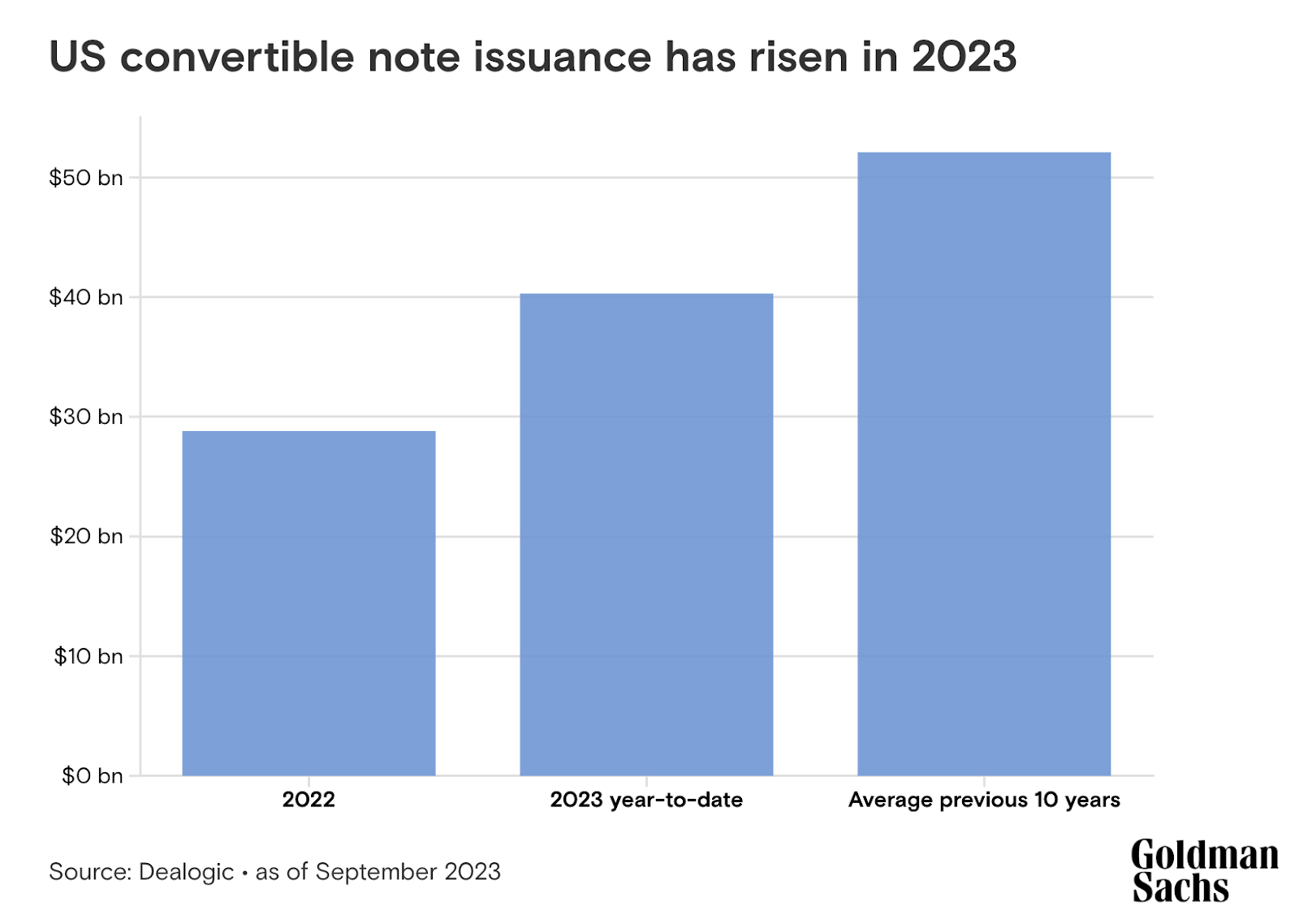

Convertible bond trend - Goldman Sachs Oct 2023 Report:

DEF Convertible Bonds: Bonds with the option to be converted to stocks

Issuance of convertible bonds increased in 2023 as interest rates increased

Attempt from companies to take advantage of the securities’ lower borrowing costs

Main companies are fast growing tech companies

Why?

Need for refinancing:

New issuers, particularly investment-grade utilities, are issuring convertibles to manage interest rate exposure

Want to reduce floating rate debt across TLs and notes, and take advantage of a lower headline coupon

Refinancing existing convertibles to push maturity dates

Higher interest rate environment

Convertibles have lower coupon than traditional bonds as they have the option to be converted to equity

Doesn’t immediate dilute shareholders’ equity: particularly attractive during periods of high interest rates when issuing traditional equity becomes more expensive

Flexibility for both sides: investors have the option to partake in equity upside while having the downside protection of fixed income instruments

2023 stats: US companies issued more than $40 billion of convertibles across 63 deals

Compared to 2022: $29 billion and 54 transactions

Comments

Post a Comment