Everything Real Estate Equity & Credit (Part I)

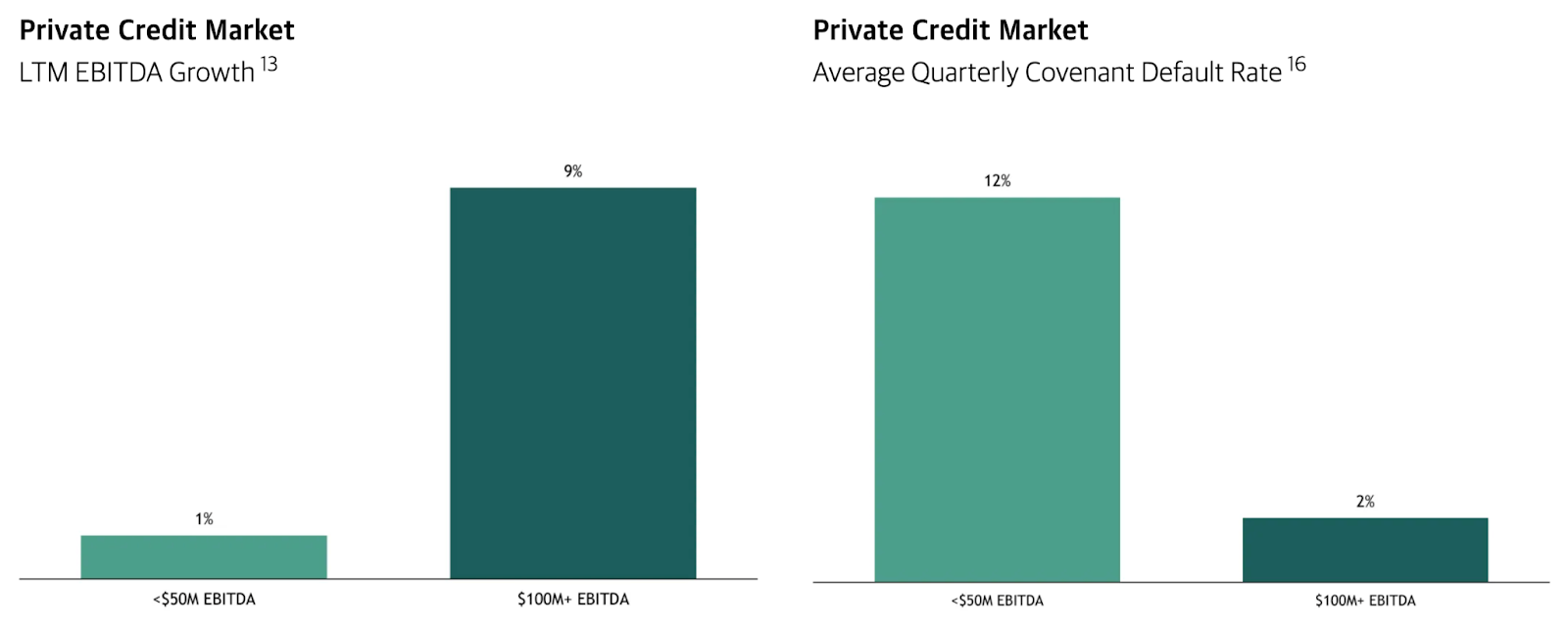

Commercial Real Estate Basics, Technicals, and Opportunities Real Estate Basics What is Real Estate Credit (Debt)? Similar to corporate private credit/direct lending, RE credit deals with the origination & management of CRE debt - Like any credit investment, RE lenders are aiming for stability in cash flows, meaning: - Large emphasis on reducing risk in terms of creditworthiness - Looking for longer-term tenant leases, diversified tenant base, strong management - Strong credit fundamentals, a track record of servicing debt and repaying principal, and healthy debt-related metrics (more on this later) - Perhaps even examine factors like covenant protection and collateral strength - Credit shops usually pursue dow